Having spent more than three decades working directly with clients in the insurance and reinsurance industry, I understand better than most the concerns raised by some insurers and brokers in response to my recent article. I appreciate that businesses are sensitive to commentary that may appear to challenge traditional distribution models or question certain market practices. However, my intention has never been to undermine the industry. On the contrary, it is precisely because I have devoted my professional life to insurance that I feel a responsibility to speak openly about transparency, informed choice and professional integrity.

Throughout my career on the direct side of the business, my focus was always on serving clients’ needs. Insurance, at its core, is not about premium volume, commission income or market share. It is about risk management and financial protection. When a client approaches an insurer or intermediary, they are often doing so at a moment of uncertainty — seeking clarity, stability and guidance. That trust carries an ethical obligation. We are not merely selling policies; we are advising on financial resilience.

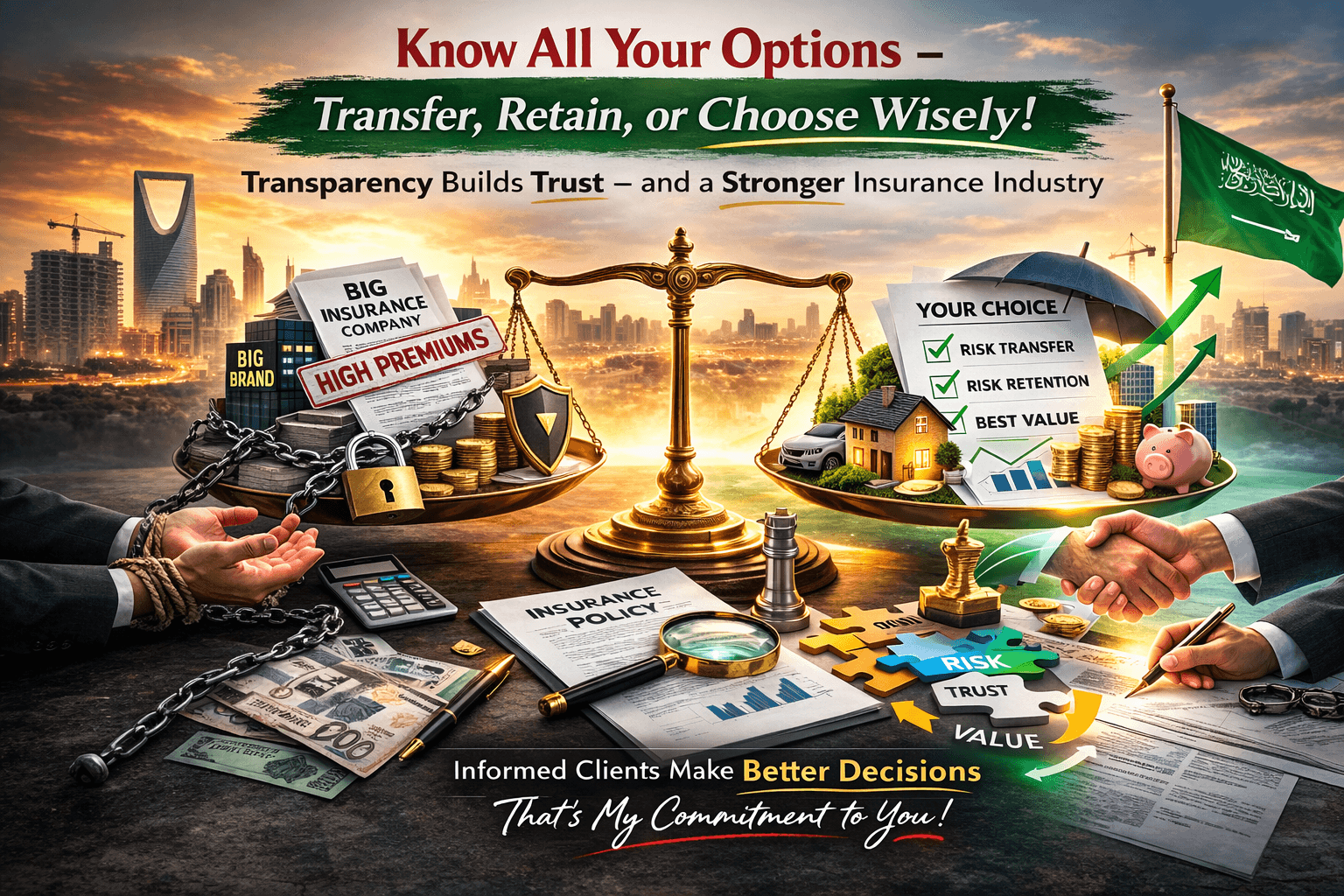

It is important to recognise that risk transfer through insurance is only one of several legitimate risk management strategies. Risk avoidance, risk reduction and risk retention are equally valid tools, depending on the circumstances. To suggest that discussing risk retention is “bad for business” is to misunderstand the broader purpose of insurance as a profession. If a particular risk can reasonably be retained without jeopardising a client’s financial stability, then it is both honest and responsible to explain that option.

In fact, providing clients with a complete picture — including when insurance may not be necessary — strengthens trust rather than weakens it. Clients are increasingly sophisticated. They understand that every business operates with commercial objectives. When professionals openly acknowledge alternatives, even those that may reduce premium income, it reinforces credibility. It signals that advice is grounded in the client’s best interest rather than purely in sales targets.

Over the decades, I have seen how long-term relationships are built. They are not built by maximising short-term revenue. They are built through candour, consistency and alignment with the client’s objectives. A client who is told, “You do not need this coverage,” or “You may consider retaining this layer of risk,” is far more likely to return when they genuinely require insurance protection. Integrity generates loyalty.

Moreover, transparency is not harmful to the insurance industry; it is essential to its sustainability. Markets that suppress open discussion about pricing, coverage scope or risk management alternatives eventually lose public confidence. By contrast, industries that embrace informed debate tend to mature, innovate and strengthen their reputations. If clients feel that information is withheld from them for commercial reasons, the damage to trust can be far greater than any short-term loss of premium.

Some may argue that highlighting deductibles, restrictive conditions or unnecessary add-ons creates discomfort. Yet discomfort is not inherently negative. It can prompt improvement. It can encourage insurers to simplify wordings, clarify exclusions and ensure that products genuinely address clients’ needs. Healthy scrutiny drives higher standards. Silence, by contrast, can permit complacency.

It is also important to separate criticism of practices from criticism of the industry itself. My observations are not an attack on insurers or brokers as professionals. Many of the finest, most ethical individuals I have known work within insurance companies and intermediary firms. My argument is not that the industry is flawed, but that clients deserve full awareness of the tools available to them. This includes understanding premiums, policy conditions, deductibles, exclusions and the possibility of structured risk retention.

After decades in direct client engagement, I have learned that informed clients make better decisions. When clients understand why they are transferring a risk — and why they are retaining another — they participate actively in the risk management process. They become partners rather than passive purchasers. This collaborative approach reduces disputes, improves claims experiences and enhances overall satisfaction.

Furthermore, openness benefits insurers and brokers who operate with professionalism. When clients are educated, they are less likely to feel misled. They are less likely to react negatively at the time of claim because expectations were clearly set at inception. Clear communication reduces reputational risk for the industry as a whole.

Ultimately, my position is guided by principle rather than profit. Having spent my career in the direct market, I am fully aware of the commercial realities of underwriting and distribution. Yet professional maturity brings a broader perspective. The long-term health of the insurance sector depends on public trust. Trust is built on transparency, fairness and informed consent.

Encouraging clients to explore all available options — including when insurance is appropriate and when risk retention may be viable — does not weaken the industry. It elevates it. It aligns our practice with the fundamental purpose of insurance: to provide meaningful protection where it is genuinely needed.

If we truly believe in the value of what we offer, we should not fear informed clients. We should welcome them. Transparency and integrity are not threats to business; they are the foundation of a resilient and respected insurance profession.

Leave a Reply